Overview

Many construction businesses and affiliates are often unaware of whether they qualify for the Research and Development (R&D) tax credit or other government tax incentive programs, or they may believe such programs do not apply to construction companies. Even those that are aware often fail to capture the full extent of the tax credits to which they are entitled.

Common Misconceptions

Oftentimes, taxpayers mistakenly believe that only professionally licensed and educated civil engineers who design innovative or revolutionary infrastructure (e.g., roads, buildings, bridges) qualify for the R&D tax credit under the U.S. tax code. However, this is not true.

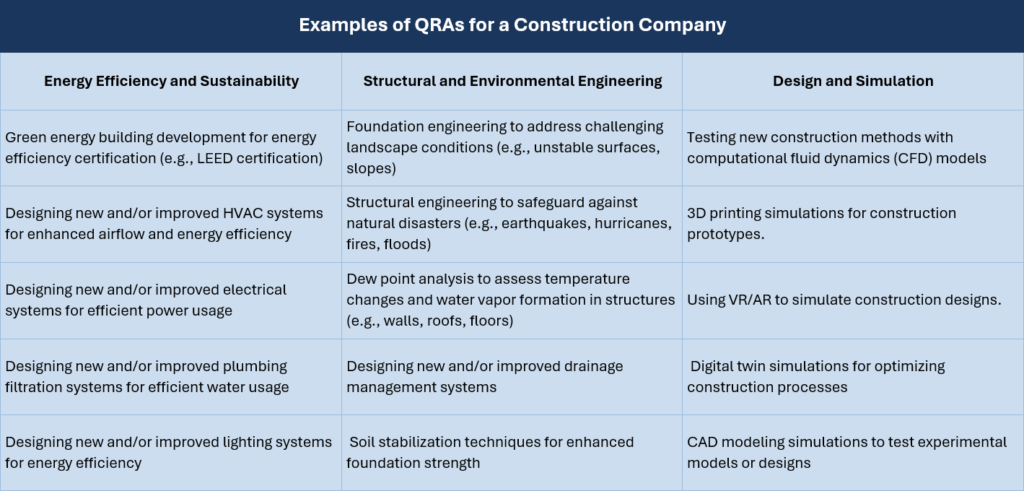

Qualified Research Activities (QRAs)

Qualified Research Activities (QRAs) refer to activities that meet specific criteria outlined by the IRS. For a construction company to qualify for the R&D tax credit, activities must pass the IRS four-part test:

- Permitted Purpose: The activity must be aimed at creating new or improved functionality, performance, reliability, or quality in a business component.

- Elimination of Uncertainty: The activity must attempt to eliminate uncertainty regarding the capability or method of developing a business component.

- Process of Experimentation: The activity must involve a process of experimentation to evaluate alternatives or test hypotheses.

- Technological in Nature: The activity must rely on the principles of engineering, physical science, or computer science.

Qualified Research Expenses (QREs)

Qualified Research Expenses (QREs) include wages, supplies, and contractor costs related to R&D activities. For construction companies, these expenses can lead to significant tax credits, allowing them to recoup a portion of their investments in innovation.

- Wages: Salaries of employees directly involved in QRAs can be claimed. Eligible roles include:

- Project Engineers: Lead efforts in developing construction solutions and experimenting with new processes.

- Superintendents and Foremen: Oversee construction projects and engage in problem-solving and experimentation to address construction challenges.

- Estimators: Analyze and model different construction approaches to optimize project execution.

- Contractor Costs: If contractors are involved in qualified research, 65% of their fees can be applied toward the credit. This applies to external consultants or engineers providing expertise in specialized areas of the project.

Supply Expenses: Supplies used in research and experimentation, such as materials for testing new construction methods or components, can be claimed. For example, construction firms may claim expenses for prototypes, testing equipment, or materials like concrete or steel that are used to develop and test new building techniques.

Case Study Example

This hypothetical example illustrates how a construction company might benefit from the R&D tax credit.

Background:

Company Name: ABC Construction

Total Technical Payroll: $190,000

QRAs Conducted:

- Developing new techniques to improve bridge construction, including evaluating alternative materials and testing structural integrity.

- Experimenting with energy-efficient building designs that meet LEED standards.

- Using CAD software to model and test new construction processes.

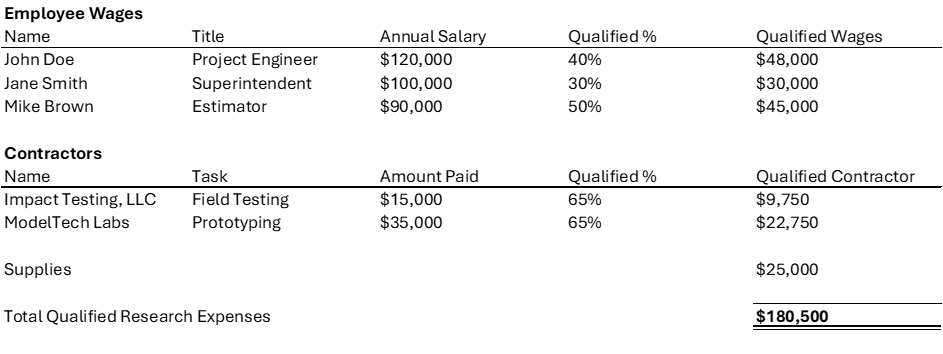

QREs Incurred:

R&D Credit Calculation:

Using the credit rate of 10% (simplified for this example), ABC Construction would receive an R&D tax credit of approximately $18,050.

Summary

For construction companies, the R&D tax credit offers significant financial benefits. By exploring qualifying activities, such as experimenting with new building techniques or developing more efficient construction processes, firms can reduce their tax liabilities and reinvest in their operations. Accurate documentation of R&D activities and related expenses is key to maximizing the credit.